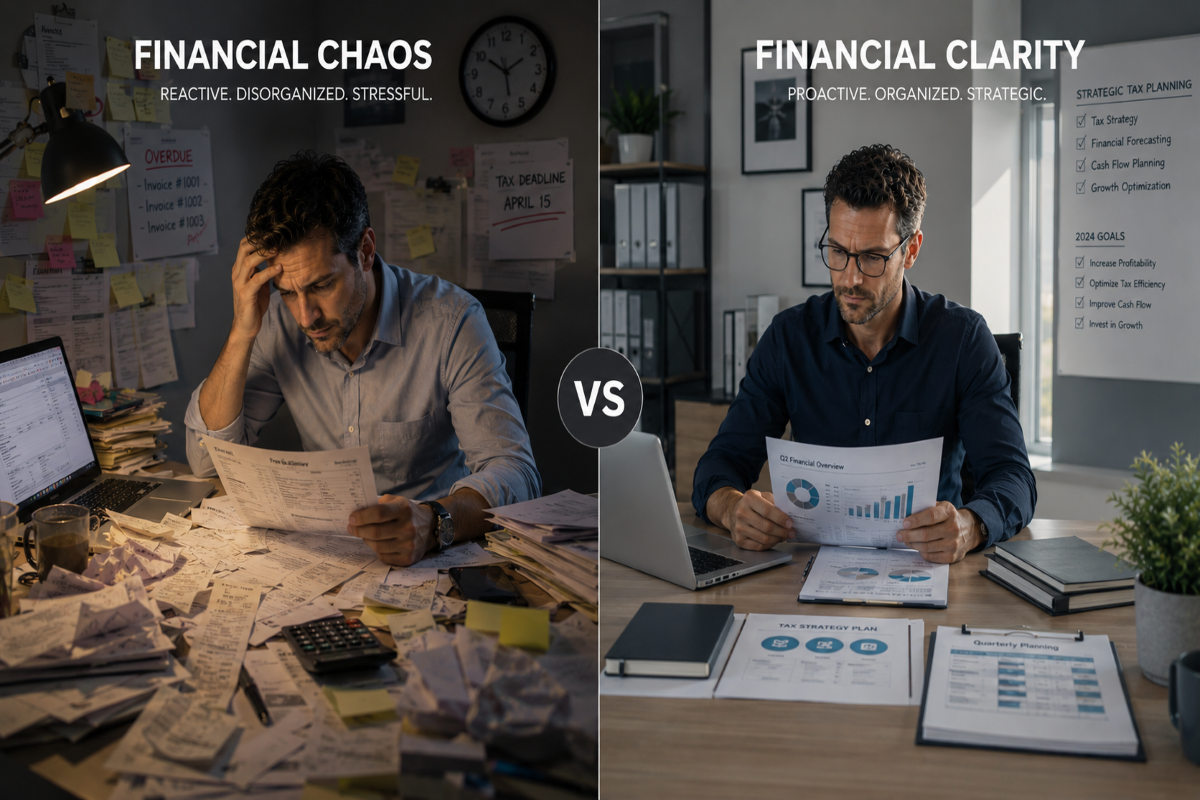

You Might Be Paying More Taxes Than You Need To

It’s 10:47 PM.

The laptop is still open.

There’s a stack of receipts on the desk, unanswered emails in the inbox, and payroll due in two days. Somewhere between client work, invoices, and trying to keep the business moving forward, bookkeeping became “something to deal with later.”

Again.

The numbers technically exist.

But they live in different places. Bank statements. Accounting software. Spreadsheets. Email threads. Half-finished notes written during busy weeks.

Tax season arrives the same way every year: fast, stressful, and heavier than expected.

So the business owner does what most overwhelmed owners do. They gather documents quickly, send everything over, hope for the best, and move on.

Then comes the tax bill.

Not shocking. Not catastrophic.

Just… bigger than expected.

Again.

And that’s the frustrating part.

Most small business owners are not careless with money. They work hard. They sacrifice weekends. They obsess over growth. They watch expenses closely.

Yet many still end up paying more taxes than necessary, not because they failed, but because the business operated reactively instead of strategically.

That distinction matters more than most people realize.

Why This Happens to So Many Small Business Owners

For many business owners, taxes feel like a once-a-year event. Something to survive, submit, and forget about until the next deadline arrives.

But overpaying taxes rarely comes from one massive mistake.

More often, it comes from small financial inefficiencies repeated quietly over time. Expenses are poorly categorized. Deductions are missed because documentation is incomplete. Decisions are made quickly during busy months without understanding their tax impact later.

None of these issues feels urgent in the moment.

That’s what makes them expensive.

A business owner might lose a few hundred dollars here, miss a deduction there, delay bookkeeping for another month, or wait until March to start thinking seriously about taxes. Individually, those decisions seem manageable.

Together, they create financial leakage that compounds year after year.

The difficult part is that many business owners assume their system is working simply because nothing appears broken. Revenue is coming in. Clients are paying. Taxes are getting filed.

So the deeper problems stay invisible.

There’s rarely a dramatic warning sign. Usually, it looks more like ongoing uncertainty:

Never fully knowing how much should be set aside for taxes

Unclear financial reports

Surprise tax bills

Uncertainty around deductions

Constantly feeling behind financially

Over time, this creates a reactive cycle.

Instead of making proactive financial decisions throughout the year, many businesses operate in survival mode until tax deadlines force attention back onto the numbers.

And by then, many tax-saving opportunities are already gone.

The businesses that reduce tax pressure most effectively are usually not chasing complicated loopholes or aggressive strategies.

They simply operate with stronger financial organization, clearer visibility, and consistent planning throughout the year.

That’s where real tax efficiency starts.

Tax Filing and Tax Strategy Are Not the Same Thing

Many business owners assume that if their taxes are filed correctly, their tax situation is under control.

That assumption makes sense. Taxes are usually treated as an annual obligation. Documents get submitted, forms are completed, and another filing season is officially finished.

But filing taxes and planning taxes are two very different processes. Tax filing focuses on reporting the past. Tax strategy focuses on shaping the future.

That distinction is where many businesses quietly lose money.

Tax Filing Is Reactive by Nature

Tax filing is designed to organize financial activity that has already happened. Revenue is reported, expenses are categorized, deductions are applied, and compliance requirements are completed.

At that stage, most financial decisions are already locked in.

The challenge is that many business owners only think seriously about taxes once filing season arrives. By then, opportunities to reduce tax liability may already be unavailable because the decisions affecting those taxes were made months earlier.

A business can technically file taxes correctly every year while still operating inefficiently from a tax perspective.

Accuracy does not always equal optimization.

Tax Strategy Happens Throughout the Year

Strategic tax planning works differently because it looks ahead instead of backward.

It examines how financial decisions made throughout the year affect long-term tax exposure. Timing, structure, payroll, purchases, retirement contributions, and expense planning all begin influencing the final outcome long before returns are filed.

For growing businesses, this becomes increasingly important.

As revenue increases, financial complexity usually increases with it. Decisions that once had minimal impact can begin carrying significant tax consequences if they are made without planning.

This is often where reactive businesses begin overpaying without realizing it.

Small Inefficiencies Become Expensive Over Time

Most businesses do not lose money through dramatic tax mistakes.

More often, overpayment happens gradually through small operational gaps that repeat year after year.

A deduction may be missed because records were incomplete. Purchases may happen at financially inefficient times. Quarterly estimates may never adjust alongside revenue growth. Bookkeeping may fall behind during busy seasons, reducing visibility into the business itself.

Individually, these issues may seem manageable.

Collectively, they create recurring financial leakage that compounds over time.

Financial Visibility Changes Decision-Making

Businesses that manage taxes effectively usually approach finances differently throughout the year.

Instead of reacting to deadlines, they maintain stronger visibility into cash flow, expenses, profitability, and future obligations. That visibility allows better decisions to happen earlier, while adjustments are still possible.

The goal is not simply avoiding mistakes.

The real advantage comes from operating proactively instead of constantly catching up.

That is where meaningful tax efficiency is usually created.

The Cost of Waiting Until Tax Season

For many small business owners, taxes only become a priority once deadlines start getting close. During most of the year, attention naturally shifts toward client work, operations, employees, sales, and keeping the business moving forward.

The problem is that effective tax planning rarely works well at the last minute.

By the time many businesses seriously review their finances, major financial decisions have already been made. Revenue has already been earned, purchases have already happened, and opportunities to reduce tax liability may no longer be available.

Reactive tax management limits flexibility. Proactive planning creates options.

Delayed Bookkeeping Reduces Financial Visibility

One of the biggest consequences of waiting until tax season is losing visibility into the business itself.

When bookkeeping falls behind, business owners often operate without a clear understanding of profitability, cash flow patterns, or future tax exposure. Decisions begin happening based on assumptions instead of accurate financial data.

This creates several common problems:

missed deductions due to incomplete records

inaccurate quarterly tax estimates

unclear cash flow visibility

difficulty tracking business expenses properly

financial decisions made without understanding tax impact

Even profitable businesses can experience unnecessary financial pressure when reporting systems are inconsistent or delayed.

Organized financial records do more than simplify filing season. They create the visibility needed for smarter business decisions throughout the year.

Last-Minute Planning Eliminates Tax Opportunities

Many tax-saving strategies depend heavily on timing.

Equipment purchases, retirement contributions, payroll adjustments, contractor payments, and entity-related decisions often need to happen before year-end to affect tax outcomes. Once filing season arrives, many of those opportunities disappear because the financial year has already closed.

This is why reactive businesses often feel frustrated during tax season.

They discover strategies after it is already too late to apply them.

Some of the most commonly missed opportunities include:

year-end deduction planning

retirement contribution optimization

strategic equipment purchases

payroll timing adjustments

entity structure evaluations

proactive quarterly tax planning

The issue is rarely a lack of effort.

More often, business owners simply did not have enough financial visibility early enough to plan effectively.

Financial Pressure Increases During Filing Season

When taxes are handled reactively, filing season becomes emotionally exhausting for many business owners.

Documents need to be gathered quickly. Accounts must be reconciled under pressure. Financial questions that should have been addressed months earlier suddenly become urgent.

That pressure creates a cycle where business owners feel:

behind on their numbers

uncertain about deductions

stressed about unexpected tax balances

disconnected from their financial position

forced into rushed decision-making

Instead of approaching tax season strategically, many businesses enter it trying to catch up.

Proactive Businesses Experience Tax Season Differently

Businesses with stronger financial systems usually experience tax season very differently.

Because bookkeeping is maintained consistently and financial reporting is reviewed throughout the year, there are fewer surprises when deadlines arrive. Tax conversations become more strategic because the business already understands its numbers long before returns are prepared.

Rather than scrambling to react, proactive businesses use tax season to confirm the effectiveness of decisions already made throughout the year.

That difference rarely comes from luck.

It usually comes from a stronger organization, ongoing visibility, and consistent planning long before filing deadlines appear.

Signs Your Business May Be Paying More Taxes Than Necessary

Many businesses overpay taxes without realizing it because the warning signs rarely look dramatic at first. In most cases, the issue develops gradually through disorganization, inconsistent planning, or limited financial visibility throughout the year.

A business may still be profitable. Revenue may still be growing. Taxes may still be filed on time.

But underneath the surface, small inefficiencies can quietly increase tax liability year after year.

Recognizing these patterns early is often the first step toward improving financial efficiency and reducing unnecessary pressure during tax season.

1. You Only Think About Taxes During Filing Season

One of the clearest signs of reactive tax management is when taxes only become a priority once deadlines arrive.

Businesses operating proactively usually review financial performance consistently throughout the year. They monitor profitability, adjust quarterly estimates, and make strategic decisions before year-end to close important opportunities.

Reactive businesses, on the other hand, often wait until filing season to begin organizing financial information.

This creates several common problems:

Missed planning opportunities

Rushed financial decisions

Incomplete expense documentation

Unexpected tax balances

Limited flexibility once deadlines arrive

Tax planning is most effective before financial decisions become permanent.

2. Your Bookkeeping Is Frequently Behind

Delayed bookkeeping creates more than administrative frustration.

When financial records are outdated or inconsistent, business owners lose visibility into the actual financial condition of the business. Profitability becomes harder to measure accurately, deductions become easier to miss, and cash flow planning becomes less reliable.

Businesses with inconsistent bookkeeping often experience:

Difficulty tracking deductible expenses

Uncertainty around profitability

Inaccurate quarterly tax estimates

Disorganized financial reporting

Increased stress during tax season

Strong bookkeeping systems support better tax planning because they create clearer financial visibility throughout the year.

3. You Are Unsure Which Deductions Actually Apply to Your Business

Many business owners know deductions exist, but are uncertain about which expenses legitimately qualify.

That uncertainty often leads to one of two problems:

Avoiding deductions out of fear of making mistakes

Claiming expenses inconsistently without proper documentation

Both situations can become expensive over time.

As businesses grow, deductions become more nuanced and interconnected with operational decisions. Vehicle expenses, home office usage, contractor payments, travel costs, equipment purchases, and retirement contributions can all affect tax outcomes differently depending on how the business is structured and documented.

Without clarity, many businesses either miss opportunities entirely or approach deductions reactively instead of strategically.

4. Your Tax Bill Feels Like a Surprise Every Year

Unexpected tax balances are often a symptom of limited financial planning throughout the year.

When business owners lack visibility into projected tax obligations, filing season becomes emotionally stressful because the final numbers feel unpredictable. Revenue may have increased faster than expected, quarterly estimates may have been inaccurate, or financial decisions may have created unintended consequences that were never reviewed proactively.

Businesses experiencing recurring surprises often struggle with:

Inconsistent cash flow planning

Underestimating tax obligations

Poor quarterly forecasting

Lack of proactive financial reviews

Reactive decision-making throughout the year

Predictability usually improves when businesses maintain stronger financial oversight year-round.

5. Financial Decisions Are Made Without Long-Term Planning

Many small business owners make financial decisions quickly because operational demands require immediate action.

Hiring employees, purchasing equipment, increasing owner compensation, changing payroll structures, or expanding operations often happens while responding to growth pressures in real time.

The challenge is that these decisions frequently carry tax implications that are overlooked in the moment.

Without proactive planning, businesses may unintentionally create:

Inefficient payroll structures

Missed deduction opportunities

Unnecessary tax exposure

Poor timing decisions

Avoidable financial inefficiencies

Strategic tax planning helps connect operational decisions to long-term financial outcomes.

That connection is what allows businesses to operate more intentionally instead of constantly reacting to surprises later.

What Proactive Tax Planning Actually Looks Like

For many business owners, “tax planning” sounds vague or overly technical. It often gets associated with complicated loopholes, aggressive strategies, or financial tactics that only apply to large corporations.

In reality, proactive tax planning is usually much simpler and more practical than that.

At its core, it means making financial decisions throughout the year with visibility, organization, and long-term awareness instead of waiting until filing season to react.

The goal is not avoiding taxes altogether.

The goal is to reduce unnecessary tax pressure while helping the business operate more efficiently.

1. Consistent Financial Visibility

Proactive tax planning begins with understanding the financial position of the business before problems develop.

When bookkeeping and reporting are updated consistently, business owners can monitor profitability, track expenses accurately, and identify financial patterns early enough to respond strategically.

This creates several advantages:

Clearer cash flow visibility

More accurate quarterly tax planning

Stronger expense tracking

Fewer surprises during filing season

Better long-term decision-making

Businesses operating with real financial visibility are typically more prepared to adapt throughout the year instead of reacting under pressure later.

2. Ongoing Tax Conversations Throughout the Year

Reactive businesses usually discuss taxes once a year.

Proactive businesses review them consistently.

That difference changes how financial decisions are made.

Instead of waiting until deadlines arrive, proactive planning creates opportunities to evaluate revenue growth, anticipated tax obligations, payroll adjustments, retirement contributions, and major purchases before year-end closes those options.

These conversations often help businesses:

Identify missed opportunities earlier

Improve cash flow planning

Adjust quarterly estimates proactively

Reduce year-end financial stress

Align operational decisions with long-term goals

Tax planning becomes more effective when it is integrated into regular business planning instead of being treated as a separate annual event.

3. Strategic Decision-Making Instead of Reactive Decisions

Many financial inefficiencies happen because business decisions are made quickly without understanding their tax impact.

This is common in growing businesses where operational demands constantly compete for attention. Owners are focused on solving immediate problems, managing employees, and maintaining growth momentum.

Proactive planning creates space to evaluate decisions before they become permanent financial outcomes.

This may include:

Reviewing entity structure as revenue grows

Evaluating payroll and owner compensation strategies

Planning major purchases strategically

Organizing deductible expenses more effectively

Improving contractor and employee classification processes

The goal is not complexity.

It is intentional decision-making supported by clearer financial awareness.

4. Reduced Stress During Tax Season

One of the most overlooked benefits of proactive tax planning is emotional relief.

Businesses operating reactively often enter tax season feeling overwhelmed, uncertain, and financially behind. Records may still need organizing, questions remain unanswered, and unexpected tax balances create additional pressure.

Proactive businesses typically experience filing season differently because much of the work has already been handled throughout the year.

That preparation often creates:

Fewer financial surprises

Cleaner reporting

More confidence in the numbers

Less deadline-related stress

Stronger overall financial control

Tax season becomes easier when businesses stop treating taxes as a once-a-year emergency.

5. Long-Term Financial Efficiency

The biggest advantage of proactive tax planning is not usually one single deduction or isolated strategy.

It is the cumulative effect of better financial habits repeated consistently over time.

Businesses that maintain organized records, review finances regularly, and plan strategically throughout the year often create stronger long-term financial efficiency because fewer opportunities are missed and fewer reactive decisions happen under pressure.

Over time, that consistency can influence:

Profitability

Cash flow stability

Financial confidence

Operational efficiency

Long-term business growth

That is what proactive tax planning is really designed to support.

Why Financial Organization Matters More Than Most Business Owners Realize

Financial organization is often viewed as an administrative task. Something operational. Something that simply keeps the business “in order.”

In reality, financial organization directly affects profitability, tax efficiency, decision-making, and long-term business stability. When financial systems are disorganized, businesses lose more than clarity. They lose visibility into opportunities, risks, and patterns that influence the company’s financial health over time.

A strong organization creates more than cleaner records. It creates control.

Clear Financial Records Improve Decision-Making

Business decisions become significantly harder when financial information is incomplete or inconsistent.

Without organized records, many owners operate based on assumptions instead of accurate financial visibility. Profit margins become difficult to track, cash flow patterns become harder to predict, and tax obligations begin feeling uncertain throughout the year.

Organized financial systems improve visibility by helping businesses:

Track profitability more accurately

Monitor cash flow consistently

Identify unnecessary expenses earlier

Understand tax exposure before deadlines

Make decisions with a clearer financial context

Strong financial organization also includes understanding how business assets are tracked, maintained, and reported over time. Businesses that improve asset visibility often gain clearer financial reporting, better operational oversight, and more accurate tax planning throughout the year.

Proper asset management for small businesses can play an important role in reducing inefficiencies and improving long-term financial control.

Disorganization Creates Expensive Gaps

Financial disorganization rarely causes one dramatic problem overnight.

More often, it creates small inefficiencies that gradually compound over time. Missing receipts, delayed reconciliations, inconsistent expense tracking, and incomplete documentation can quietly increase financial pressure year after year.

These gaps often lead to:

Missed deductions

Inaccurate reporting

Avoidable tax overpayments

Increased filing stress

Reduced financial confidence

The challenge is that many businesses normalize this chaos because they become accustomed to operating under constant pressure.

What feels “manageable” operationally may still be financially inefficient.

Consistent Systems Reduce Tax Season Stress

Businesses with organized financial systems usually experience tax season very differently from reactive businesses.

Because records are already updated and categorized consistently throughout the year, filing preparation becomes smoother and more predictable. Questions are easier to answer, documentation is easier to access, and financial reports provide clearer insight into the business itself.

This level of organization often creates:

Faster filing preparation

Fewer financial surprises

More accurate reporting

Improved communication with accountants

Reduced deadline-related stress

Tax season becomes less overwhelming when financial organization is maintained proactively instead of being rushed at the last minute.

Financial Visibility Supports Long-Term Growth

As businesses grow, financial complexity grows alongside them.

Payroll structures, contractor payments, equipment purchases, operational expenses, and tax obligations all become more interconnected over time. Without organized systems, it becomes increasingly difficult to manage growth efficiently because the business loses visibility into how decisions affect long-term profitability.

Organized financial management supports growth by creating:

Stronger forecasting capabilities

Clearer profitability analysis

More strategic tax planning

Better operational visibility

Improved long-term financial control

Growth becomes more sustainable when businesses understand not only how much revenue they generate, but also how efficiently they operate financially.

By improving financial organization, businesses create a stronger foundation for both daily operations and long-term decision-making. Over time, that clarity often becomes one of the biggest advantages a business can develop.

Financial Visibility Changes Everything

Most business owners do not intentionally neglect their finances.

In fact, many work extremely hard to stay responsible. They track expenses as best they can, try to stay organized during busy seasons, and make financial decisions while balancing dozens of operational demands at the same time.

The challenge is that small financial inefficiencies tend to compound quietly.

A missed deduction may not seem significant this year. Delayed bookkeeping may feel manageable during a busy quarter. Reactive tax planning may appear harmless when deadlines are still months away.

But over time, those patterns begin affecting profitability, cash flow visibility, financial confidence, and long-term business efficiency.

That is why businesses that manage taxes effectively usually approach finances differently.

They do not wait for filing season to understand their numbers. They maintain visibility throughout the year, organize financial systems proactively, and make decisions with a clearer understanding of how those choices affect future tax outcomes.

The goal is not perfection.

It is creating enough financial clarity to operate proactively instead of constantly reacting under pressure.

Better Financial Visibility Creates Better Business Decisions

Many business owners think tax efficiency starts with deductions.

In reality, it often starts much earlier with visibility and organization.

When businesses understand their financial position clearly, they are better equipped to:

Identify inefficiencies early

Plan for future tax obligations

Improve cash flow management

Reduce financial surprises

Make more strategic operational decisions

Financial clarity affects far more than tax filing alone. It influences how confidently a business can grow, invest, hire, and plan long-term.

Proactive Planning Reduces Unnecessary Pressure

One of the biggest benefits of proactive financial management is reduced stress.

Reactive businesses often experience constant financial uncertainty because important decisions happen under pressure. Filing deadlines become overwhelming, reporting feels rushed, and tax obligations feel unpredictable.

Proactive businesses typically experience greater stability because financial systems are maintained consistently throughout the year.

This often leads to:

Fewer last-minute surprises

More predictable tax planning

Stronger financial control

Cleaner reporting systems

Greater confidence in decision-making

Over time, that consistency creates both operational and financial advantages.

The Real Advantage of Proactive Tax Planning

Paying taxes is part of running a successful business.

Paying more than necessary because of disorganization, limited planning, or poor visibility does not have to be.

Many businesses improve tax efficiency not through aggressive tactics, but through stronger financial habits repeated consistently over time. Better bookkeeping, clearer reporting, proactive planning, and earlier decision-making often create meaningful long-term improvements without adding unnecessary complexity.

That process usually starts with one important shift:

Moving from reactive financial management to proactive financial awareness.

And for many businesses, that shift changes far more than just the tax bill.

Sometimes the biggest financial opportunities are the ones businesses never realize they missed. A second opinion on your current tax and financial strategy can often reveal gaps, inefficiencies, and opportunities that may be quietly affecting your bottom line.